How much does critical illness cover cost?

We’d love to give you an upfront cost for your critical illness cover. But we know that everyone is different, and this can change the cost of your monthly premiums.

Insurers will base their premiums on several different factors including:

Your age

weight and health

smoker or non-smoker

medical history

family history

your job

amount of cover and for how long

Let’s look at two hypothetical examples of customers seeking critical illness cover:

Critical illness insurance example cost #1

Bridget is 35 years old. She is a single mum with two children. She works as a nurse. She wants to buy critical illness insurance with a pay out of £100,000. She has no pre-existing medical conditions or family history of critical illness. She doesn’t smoke and is healthy. She chooses a level term policy over 20 years.

Bridget’s monthly premium is £30.31. She would pay £363.72 per year.

£30.31 per month | £100k payout

Critical illness insurance example cost #2

Robert is 45 years old. He is married. He works as an architect. He wants £150,000 of critical illness cover for 15 years. He has high blood pressure and high cholesterol. Both are controlled by medication. He has a family history of heart disease. He chooses a decreasing term.

Robert’s monthly premiums are £56.40. He would pay £676.80 per year.

£56.40 per month | £150k payout

Whatever your circumstances, we are confident that we can find you a suitable critical illness plan. What’s more, with our price promise guarantee, you can feel confident that you won’t find a better price anywhere else.

Everything we do is about finding you the best possible protection, for the lowest possible price.

Life insurance cost, case study.

James is looking for life insurance to cover his mortgage and to give a lump sum to his wife and two children. James had a stroke ten years ago but doesn’t suffer from any symptoms.

We found James the increasing policy below:

Total Cover

Amount:

£750,000

Monthly Premium

Cost:

£41.57

Duration of

Policy:

Until age 70

All you need to know about critical illness cover

Critical illness insurance pays out a lump sum if you’re diagnosed with one of the illnesses covered by your policy. The lump sum can be used to pay for:

your mortgage or rent

household bills

medical expenses

ifestyle changes caused by your illness

or anything else that your family needs to spend money on.

Critical illness insurance is different from life insurance and income protection insurance. Life insurance pays a lump sum if you die. Income protection insurance provides a regular income if you can’t work because of illness or injury. Critical illness insurance covers serious illnesses, like cancer, heart attack, or stroke.

The amount of cover and policy length that you need will depend on your personal circumstances. Ask yourself:

How much would it cost to cover your essential expenses if you’re diagnosed with a serious illness

How much would it cost to cover any extra costs

Is the length of cover reliant on an event, like retirement or paying off your mortgage

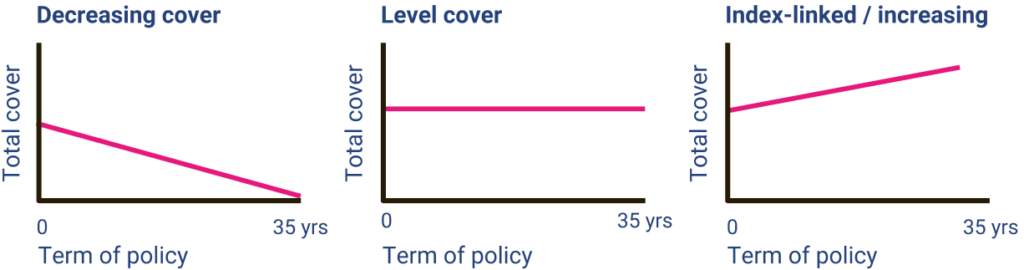

There are two types of critical illness cover. With level term, your premiums remain the same for the entire policy. If you choose decreasing term, your monthly payments reduce over time. Level term cover is generally more expensive. It also offers more protection and flexibility.

We don’t expect you to know the full details of each type of policy.

That’s what we’re here for.

With our support, we can talk through the various options and help you decide which type is best for you. We’ll answer all your questions, and make sure that you fully understand how critical illness works, and how it can support your finances.

Is it a stand-alone policy, or is it part of a life insurance plan?

Critical illness cover can be bought as a standalone policy or as an add-on to your life insurance. A standalone policy means you can choose the amount and length of cover, independent of your life insurance. You can also keep your critical illness policy even if you cancel your life insurance.

If you add critical illness cover to your life insurance policy, you pay one premium for both. This may work out cheaper and you can benefit from the same terms and conditions for both.

We know that everyone is different. For some people, the stand-alone policy is better suited, while others may find that the life plan add-on is what they are looking for.

We will always make sure that you’re choosing the right policy for YOU.

We’ll always check that you’re getting maximum protection for minimum prices.

Can you take out critical illness insurance if you have a complicated medical history?

Your medical history doesn’t have to mean a ‘no’. If you have a complicated medical history, critical illness cover will be more expensive. However, we’re confident we can find you the best fit policy for your needs.

Our relationships with niche insurers across the UK mean that we can usually find a positive solution for people, even with the most complex medical histories.

We will do whatever we can to help you protect your family and stabilise your finances.

All you need to do is focus on your health.

Critical illness insurance for the self-employed

If you’re self-employed, you don’t get work benefits like sick pay. If you develop a serious illness that stops you from working, you may have to rely on your savings to support your family.

Research by LV= found that 41% of self-employed workers have no savings at all, and 28% would be forced to rely on family if they couldn’t work.

If you’re self-employed, critical illness insurance can provide valuable financial protection and peace of mind, should you face a devastating diagnosis.